海外研报

筛选

On Our Minds RBI: Growth optimism behind hawkish stance

The RBI kept the policy rate (at 6.5%) and the policy stance (withdrawal of accommodation) unchanged during its monetary policy meeting in August

海外研报

2024年08月12日

Some relief, however the risks still remain

The market began the week with a broad-based risk-off sentiment on Monday, and the continued carry trade unwinding pushed the USD/JPY and USD/CNY

海外研报

2024年08月12日

European Contextual Diary The Week Ahead

In this note we preview the coming week's corporate events Below we highlight three key events for next week. Please see this excel for a full list of

海外研报

2024年08月12日

UK Weekly Kickstart Summer data-only update

General disclosuresThis research is for our clients only. Other than disclosures relating to Goldman Sachs, this research is based on current public

海外研报

2024年08月12日

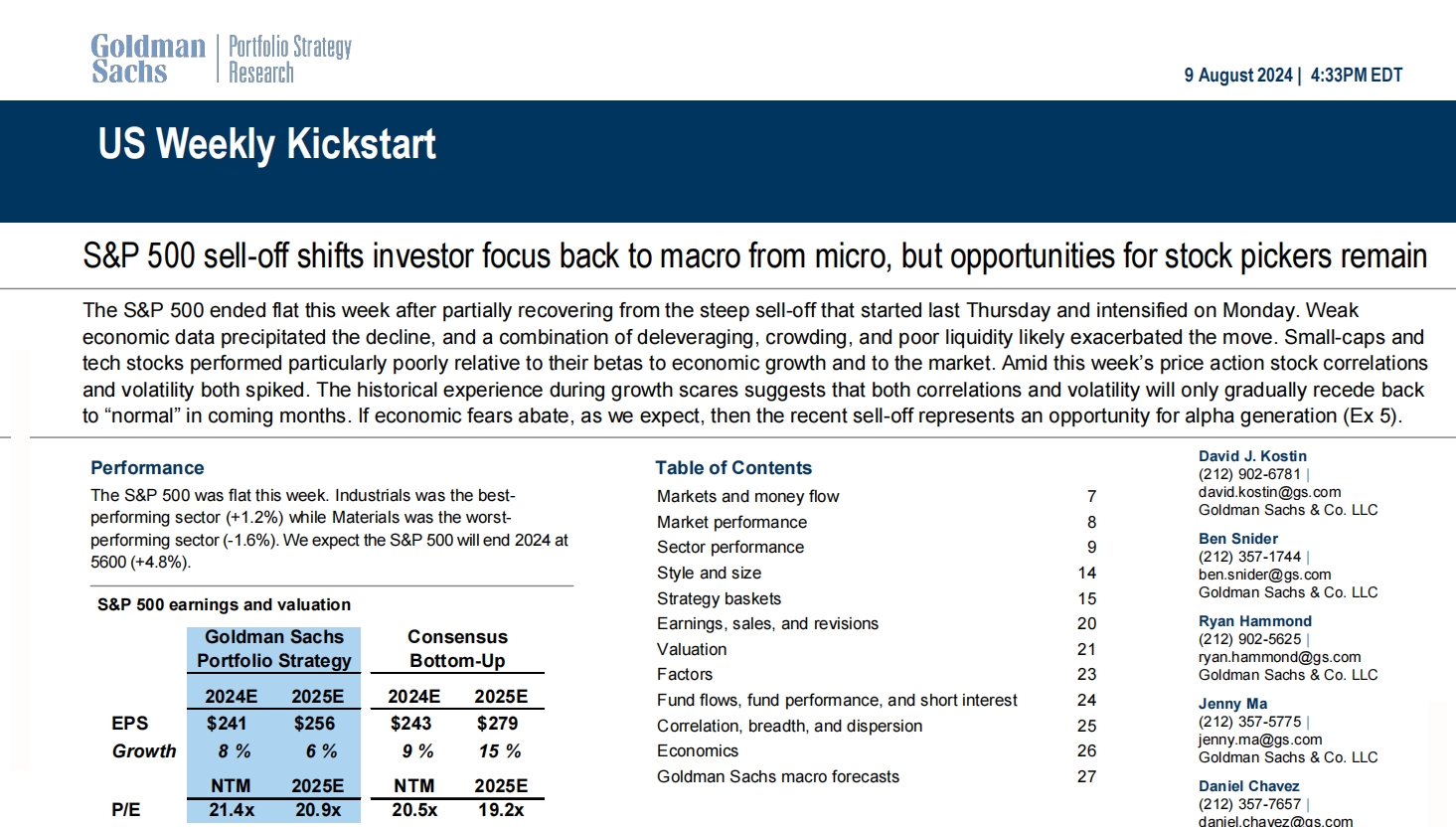

US Weekly Kickstart

The S&P 500 ended flat this week after partially recovering from the steep sell-off that started last Thursday and intensified on Monday. Weak

海外研报

2024年08月12日

Mizuho China Weekly Outlook

China’s CPI rose by 0.5% YoY in July, surpassing market expectations. However, this uptick in the inflation rate was helped by stabilizing food prices rather than improved consumer demand. Food prices in July

海外研报

2024年08月14日

Total recall 2Q:24 – Core strength drives OEMs; Supplier outlooks disappointing

Pricing remains solid but production outlook down YoY2Q:24 showed a change of pace for the automotive industry. Global production is now

海外研报

2024年08月14日

Consumer Checkpoint Facing hurdles or the high jump?

• Bank of America aggregated credit and debit card spending per household fell 0.4% year-over-year (YoY) in July, compared to a

海外研报

2024年08月14日

Back to fundamentals

Rates investors will focus on PPI, CPI and retail sales this week, whichwill fine-tune expectations for the September FOMC meeting.

海外研报

2024年08月14日

What next after a volatile week for markets?

The period of relative calm for markets came to a screeching halt overthe last week or so. But while recent market moves have been dramatic,

海外研报

2024年08月14日